OIA Members Make Significant Progress in 2024

In 2024, 84 OIA members participated in the Climate Action Corps (CAC) and/or the Clean Chemistry and Materials Coalition (CCMC). These programs are designed to support outdoor companies in reducing their impacts on the planet. Companies of different sizes, product categories, and geographic locations came together with the goal of working together to leave our planet better than we found it and to protect the outdoor experience upon which we all depend. Each program has a pathway for reducing impacts and achieving programmatic goals (learn more about our programs here). This blog takes a deeper dive into the member stories and successes from 2024.

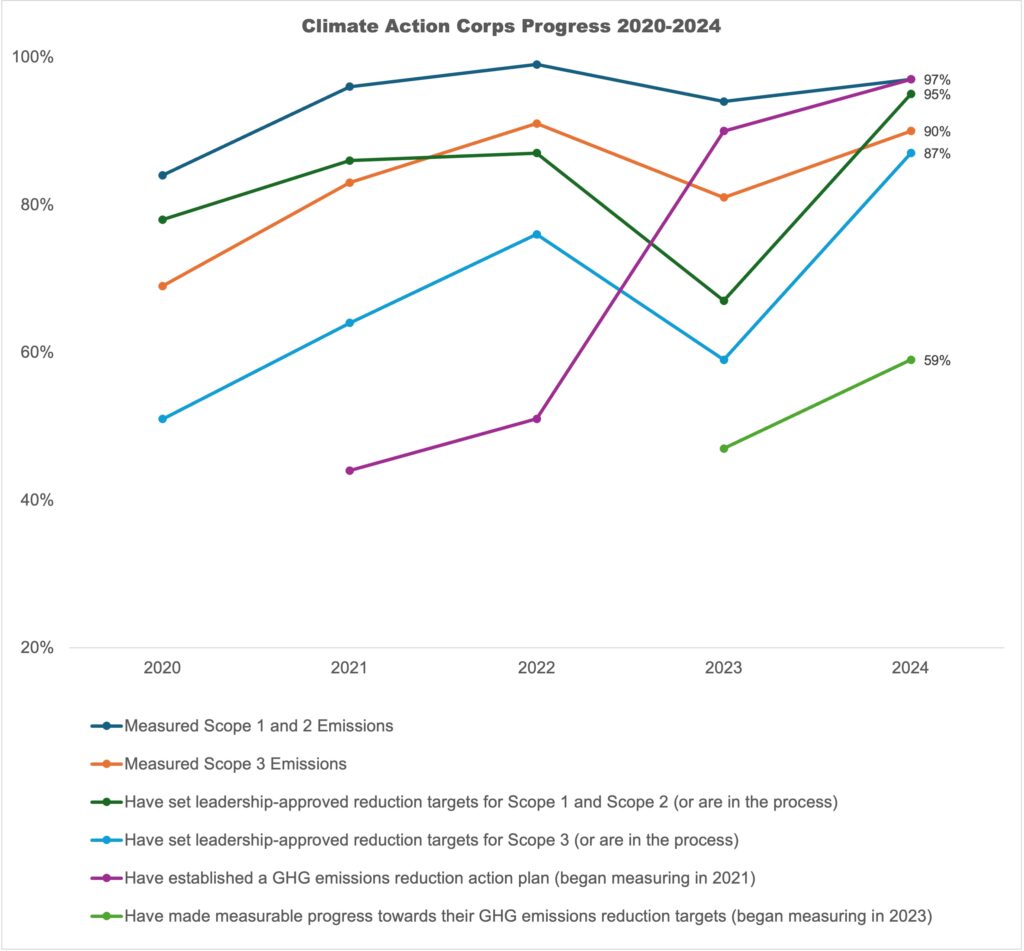

Climate Action Corps 2024 Progress: Five Years of Impact Throughout the Value Chain

In the fifth year of tracking member progress, the CAC continues to make great progress along the pathway of measuring greenhouse gas (GHG) emissions, setting GHG emission reduction targets, and making GHG reductions across emission scopes. Compared to 2023, CAC members increased their progress on average by 15% across all major tracked categories. Here is a snapshot of the cumulative progress CAC members have made (note – there are some data discrepancies that account for inflated percentages in 2021 and 2022 that were remedied in 2023 and going forward):

Here is the progress that CAC members made in 2024:

- 97% have measured their company’s Scope 1 and Scope 2 emissions (or are in progress or have an initial estimate)

- Scope 1 emissions are a company’s direct emissions from owned or controlled sources. Examples of these include combustion of fuels, fugitive emissions, etc.

- Scope 2 emissions are indirect emissions from a company’s purchased energy generated off-site. The main example is electricity.

- 90% have measured their company’s Scope 3 emissions (or are in progress or have an initial estimate)

- Scope 3 emissions are a company’s indirect emissions that occur in the value chain, including both upstream and downstream emissions. Examples of these include purchased goods & services, third-party logistics, business travel, etc.

- 95% have set leadership-approved reduction targets for Scope 1 and Scope 2 (or are in the process)

- 87% have set leadership-approved reduction targets for Scope 3 (or are in the process)

- 97% have established a GHG emissions reduction action plan (or are in the process) that guides efforts to achieve their targets

- 59% have made measurable progress towards their GHG emissions reduction targets

Going Beyond the Numbers

REI’s total 2024 emissions (Scopes 1, 2 and 3) were 12.2% lower than emissions in their 2019 baseline year. They achieved this reduction through:

- 100% renewable energy

- Lower-carbon materials

- Reducing emissions from REI Co-op product manufacturing

- Engaging retail brand partners to reduce emissions

- Reduced emissions from international freight

- Expanding clean energy procurement resources with manufacturing partners

- Providing expertise, knowledge, and tools to accelerate supplier decarbonization

- Investing in Southeast Asia’s clean energy ecosystem

In 2024, Klean Kanteen’s scope 1 and 2 emissions were 74% below their base year level in 2016 and scope 3 emissions were 86% below their base year level in 2019. Some actions Klean took to reduce their emissions include:

- Produced or procured renewable electricity (and/or renewable energy credits) for their owned/controlled facilities

- Engaged with their suppliers about energy efficiency

- Engaged their suppliers about measuring their GHG emissions

- Changed their company’s products and materials to alternatives with lower-GHG footprint

L.L.Bean achieved a 22% absolute reduction in scope 1 and 2 emissions from 2019 to 2024. They decreased their scope 1 emissions significantly by investing in a new headquarters and electrifying their primary heat source, which was previously natural gas. In addition, L.L.Bean has made energy-efficient investments resulting in an overall decrease in Scope 2 emissions across stores, their fulfillment center, and HQ. Examples include switching to energy efficient lighting, compressors, and HVAC units. Warmer winters and the increase of renewable energy in the New England power grid have also supported their Scope 2 reduction. L.L.Bean plans to retire Renewable Energy Certificates to reach the overall 50% reduction by the end of 2025, through their participation in 16 renewable energy projects across Maine.

Rab USA’s 2024 carbon accounting data showed a 47% reduction in total emissions from a 2019 baseline. This reduction includes a 66% reduction in purchased goods and services in their scope 3 emissions through collaborating with their supply chain. Rab’s overall emissions have fallen due to three significant changes in the last year:

- Adoption of renewable energy in tier 1 suppliers

- Reduction in production figures due to a focus on reducing stock levels within their supply chain.

- Switching to primary production data rather than secondary data to improve their raw materials’ GHG emissions calculator methodology

We look forward to supporting our members’ progress to make greater, measurable reductions in GHG emissions, despite external economic and regulatory pressures facing the industry and our supply chains.

See Climate Action Corps members’ individual 2024 progress here.

Clean Chemistry and Materials Coalition 2024 Progress: Members Show Leadership in Inaugural Reports

2024 was the first year OIA asked members of the Clean Chemistry and Materials Coalition (CCMC) to report on their progress. In the inaugural progress reports, CCMC members showed company commitments to cleaner, safer chemistry. Since the inception of CCMC in Summer 2023, the outdoor industry has come together to phase out per- and polyfluoroalkyl substances (PFAS), champion safer chemistry in the supply chain, and switch to safer chemical and material alternatives when possible. Creating a robust chemicals management system is a long and complex process, but CCMC members have already achieved the following:

- 80% have set goals related to chemicals management

- 67% have an action plan that guides efforts to achieve their chemicals management goal(s)

- 92% have communicated their RSL to finished goods suppliers, representing 95% or more of their production volume

- RSL = Restricted Substances List

- 71% have communicated their RSL to materials suppliers, representing 95% or more of their production volume

- 57% have engaged with many finished goods suppliers about implementing a chemicals management system

- 41% have engaged with many materials suppliers about implementing a chemicals management system

Going Beyond the Numbers

Cotopaxi, through a strategic approach to material sourcing and internal due diligence testing, is confident that as of 2024, its products contain no intentionally added PFAS. However, Cotopaxi recognizes that current PFAS testing methodologies have yet to fully align with evolving regulatory standards, and they continue to assess and refine their verification processes to ensure the highest level of accuracy.

VF Corporation, the parent company of CCMC members Altra™, Smartwool™, Timberland™, and The North Face™, has a robust, proprietary chemicals management program called CHEM-IQ. Through this program, VF has committed to eliminating and/or restricting 100% of unwanted chemicals or substances from VF’s supply chain by FY26. Through CHEM-IQSM, VF has identified and removed more than 1,330 MT of non-preferred chemicals from its supply chain. In FY2024, 420+ supply chain factories participated in the CHEM-IQ program.

YETI has an extensive restricted substances list (RSL) that provides clear and concise guidance to enable responsible product development and chemical management within its supply chain. Their RSL specifies the chemical restrictions applicable to substances used in manufacturing YETI components, products, and packaging. In addition, it outlines the responsibilities of suppliers to YETI and identifies resources available for support. YETI has also phased out long-chain PFAS and its derivatives, bisphenols and their derivatives, and was on track in 2024 to phase out short-chain PFAS and their derivatives, and PVC (excluding promotional stickers, window decals, and select international accessories).

See Clean Chemistry and Materials Coalition members’ individual 2024 progress here.

How OIA Helped Members Achieve Their Goals in 2024

In 2024, the OIA Sustainable Business Innovation team expanded our resources and collaboration offerings for our members to help them achieve their goals in climate and chemistry. We introduced task forces in the spring to give members the opportunity to collaborate on a climate or chemistry topic, without any additional financial investment. These task forces addressed issues like PFAS testing, sourcing low-impact aluminum, tracking sustainability regulations, and more. Our past and current task forces include:

- Hardgoods Task Force: developed a resource for all OIA sustainability members, outlining potential chemical contamination hotspots in hardgoods.

- PFAS Testing Task Force: investigated which materials were most likely unintentionally contaminated with PFAS. An executive summary of those findings is available to all OIA members.

- Aluminum Task Force (ongoing): guidebook to source low-carbon aluminum

- Content Claims Standards Task Force (ongoing): Creating a guidebook to support finished goods manufacturers with Textile Exchange’s Content Claim Standard implementation.

- Chemical Risks for Recycled Materials Task Force (ongoing): creating a guidebook to understand the risks of chemical contamination from recycled feedstocks.

- Compliance Reporting Task Force (ongoing): supporting members with state and federal reporting requirements throughout the year.

- Supplier Climate Principles Task Force (ongoing): creating a collective approach for engaging with suppliers to reduce emissions.

- Sustainability Policy Task Force (ongoing): supporting sustainability compliance and advocacy at the state, federal, and international levels.

We also continued our Impact CoLabs in 2024 – collaborative, pre-competitive, emissions reduction initiatives led by OIA and service providers to help members meet their sustainability goals more efficiently through collaboration. Learn more about Impact CoLabs here. Here are the CoLabs we offered members in 2024:

- Clean Heat: decision support tool to electrify heating in textile facilities

- Vietnam Renewable Energy: group solar procurement with brands and manufacturers

- Carbon Leadership Project: carbon reduction roadmaps for apparel manufacturers

- Virtual Power Purchase Agreement: group procurement of renewable energy

- Drinkware: carbon reduction roadmaps for drinkware manufacturers

- Tent Flammability: change policy to no longer require dangerous flame retardants in tents

- Electrifying the Textile Industry: feasibility study to understand challenges and opportunities of electrifying the textile industry

The OIA Team also released additional resources in climate and chemistry, and advocated on behalf of our industry in Vermont, Colorado, Maine, Washington, and California (PFAS and Climate). We held 12 webinars, 12 Campfire Chats (member-led discussions on a sustainability topic), and 24 technical and legislative office hours for our members. Finally, we held our inaugural Catalyst Conference in Seattle, WA, and gathered 175 outdoor industry professionals in person for the first outdoor sustainability-centered event since 2019. At this conference, sustainability practitioners of all levels discussed GHG reduction, green marketing strategies, chemicals management, and more. We were thrilled to gather with our community and tackle important issues in climate and chemistry together.

We are incredibly proud of our members’ progress in 2024 and look forward to the continued trend of positive progress from our industry in climate action and safer chemistry. The trail to a more sustainable future can be bumpy, but with the collective force of the outdoor industry, we can lead in creating a more sustainable future. Join us.

Data Disclaimer: OIA does not verify member progress report claims. Members report on their own progress, and give OIA permission to share publicly. Some GHG reductions reported may be the result of a decline in business, or other externalities that caused a drop in emissions unrelated to specific member reduction actions.